News & Media

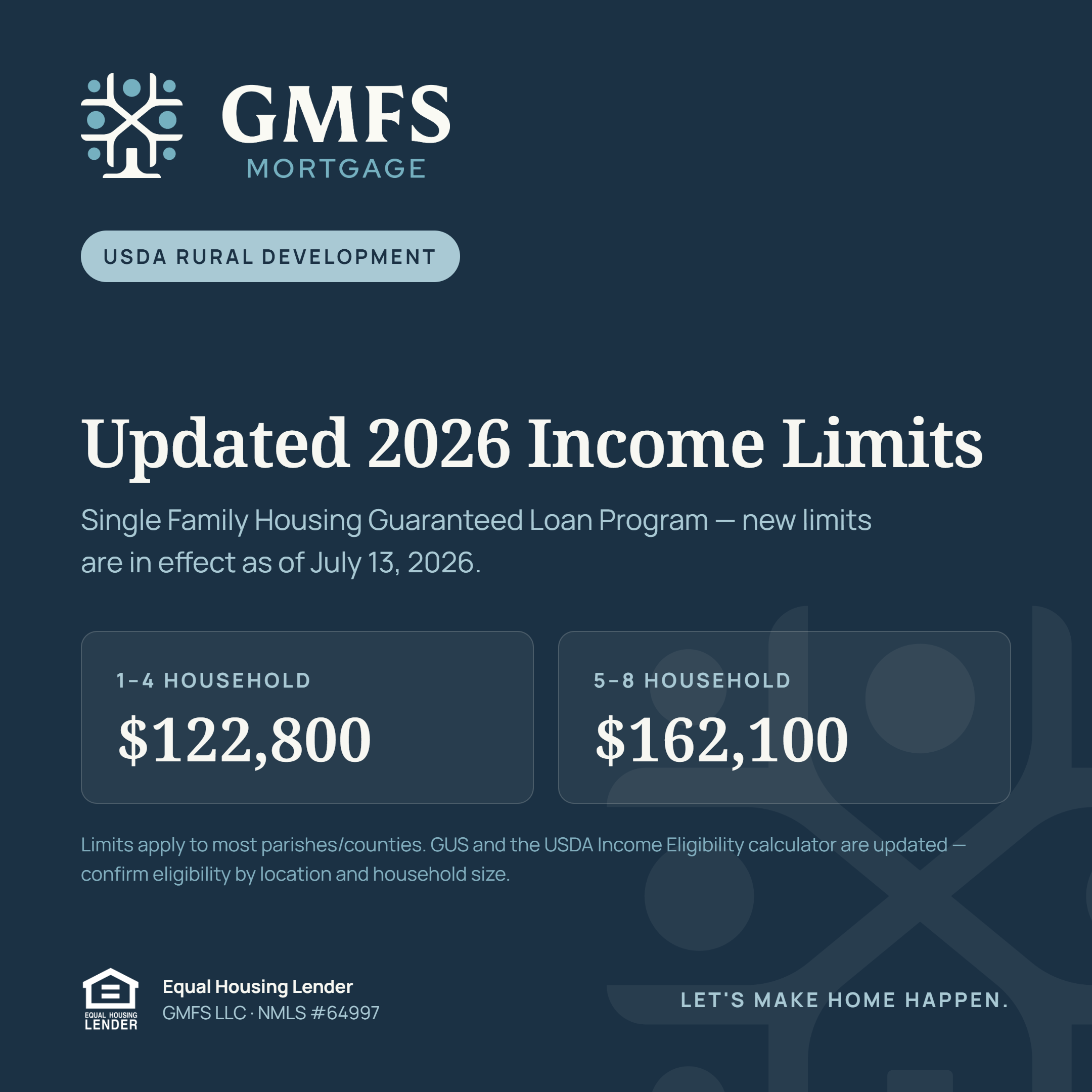

USDA Rural Development Income Limits 2026

USDA Rural Development increased Income Limit for the Single Family Guaranteed Loan Program in 2024. Get pre-qualified today!

USDA Rural Development Income Limits 2026