Celebrating Our 2025 Chairman’s Club – People’s Choice Top Performers

$2,500 HomeReady & Home Possible Grant Available for 2026

GMFS Bluebonnet Branch Opens with a Mardi Gras Celebration

Lindsay Huff and Jan Hardin Earn Certified Veterans Lending Specialist Designation

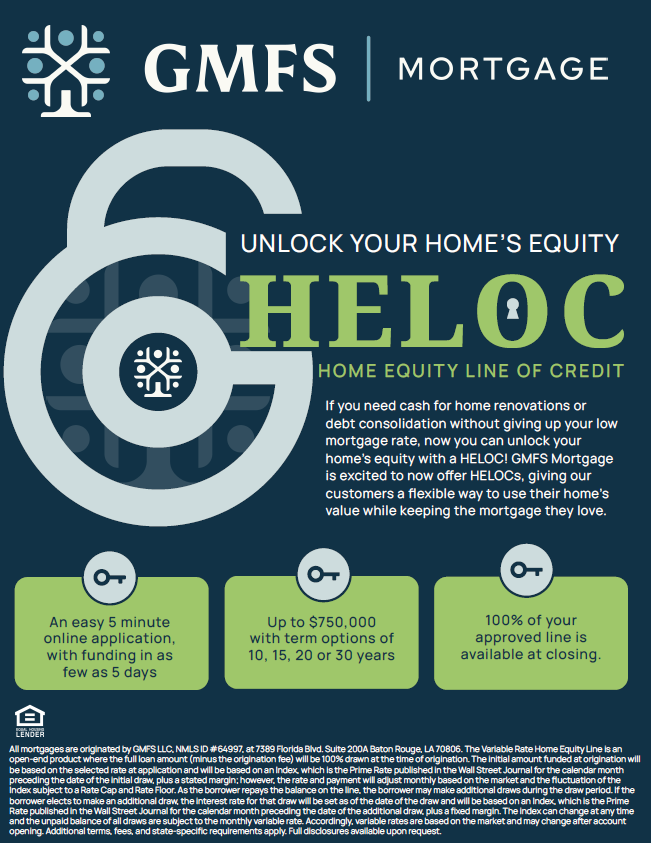

GMFS Mortgage Now Introducing a Home Equity Line of Credit (HELOC)

Introducing the 2025 GMFS Chairman’s Club- Top Producers

Celebrating Stacey Britton’s Continued Leadership with the Acadiana Mortgage Lenders Association

Congratulations to Mimi Mire on Her Election to the Louisiana Home Builders Association Leadership Team

GMFS Mortgage Supports MBA’s Mortgage Banking Bound Program at LSU

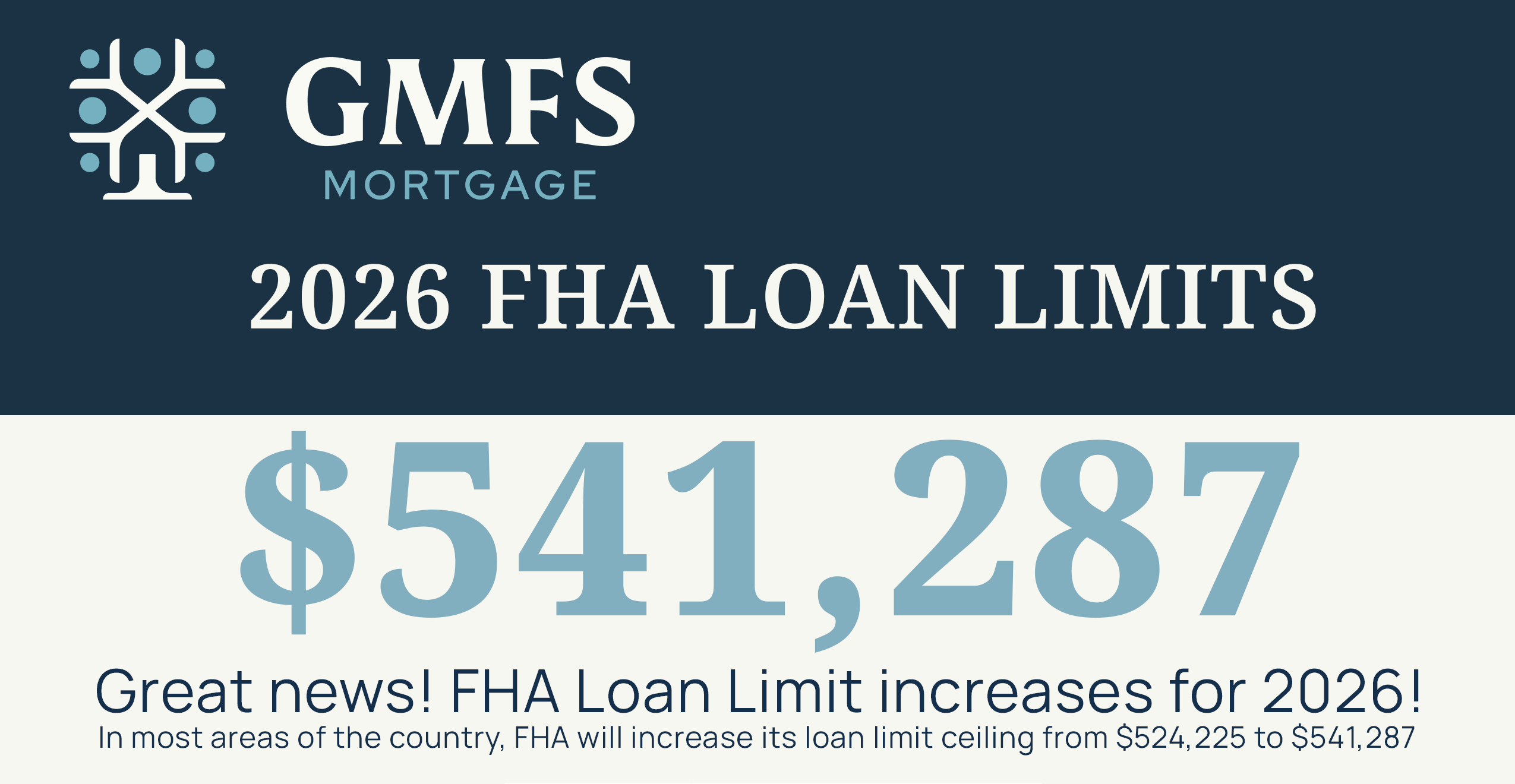

2026 FHA Loan Limits

Helping 8,200 Veteran Families and Counting: GMFS VA Loan Advantage

New 2026 Conventional Loan Limits